Pakistan has secured its first sovereign rating upgrade in six years, a symbolic return from the brink of default. Yet market experts warn the country’s economic recovery remains fragile and deeply reliant on external support.

Fitch Ratings upgraded Pakistan’s long-term foreign currency rating from ‘CCC+’ to ‘B-’ with a stable outlook in April, acknowledging fiscal progress under the country’s latest IMF program. The upgrade reflects renewed investor confidence in Pakistan’s macroeconomic management following a near default crisis in 2023 that sent borrowing costs soaring and pushed the country to the brink of financial collapse.

According to the Fitch report, the upgrade reflects “increased confidence that Pakistan will sustain its recent progress on narrowing budget deficits and implementing structural reforms.’’

However, Fitch also cautioned that “implementation risks remain, and financing needs are still large,’’ pointing to the ongoing challenges Pakistan must navigate.

This mixed outlook suggests that while international confidence is returning, sustained reforms and careful fiscal management will be critical to maintaining momentum and avoiding setbacks.

Market Response Shows Cautious Optimism

The rating upgrade triggered an immediate but measured market response. The KSE-100 index gained 385 points (0.33%) on April 15, closing at 116,775.50 as domestic investors responded to the positive signal.

However, Pakistan’s borrowing costs remain significantly elevated compared to regional peers, with Moody’s projecting that interest payments will consume nearly 40% of the country’s 2025 budget, according to an April 18 report from Business Recorder. This debt burden represents a stark contrast to the 13% median for ‘B-’ rated peers, highlighting the substantial fiscal constraints Pakistan continues to face despite its improved rating, as detailed in Pakistan’s Debt Sustainability Report FY2025-FY2027.

IMF Program Delivers, But Implementation Risks Loom

The upgrade primarily stems from Pakistan’s adherence to recent IMF benchmarks and several measurable improvements:

- Fiscal deficit projected to narrow to 6% of GDP in FY25(from nearly 7% in FY24)

- Primary surplus expected to more than double to over 2% of GDP

- Foreign exchange reserves rebounded to nearly $18 billion in March 2025, up from less than $8 billion in early 2023

- Current account posted a $700 million surplus in the first eight months of FY25

The March 2025 staff-level agreement with the IMF on a $7 billion Extended Funded Facility and a new $1.3 billion Resilience and Sustainability Facility has reinforced confidence in the country’s economic reforms and policy direction according to the IMF. The recent IMF review has acknowledged Pakistan’s progress in implementing structural reforms and meeting fiscal targets. Despite this progress, the review pointed out persistent economic risks, including elevated public debt levels, limited fiscal space, and structural challenges that could impede sustainable growth. While the fiscal support signals confidence in Pakistan’s reform agenda, the IMF stressed the need for continued reform efforts to secure enduring economic stability and growth.

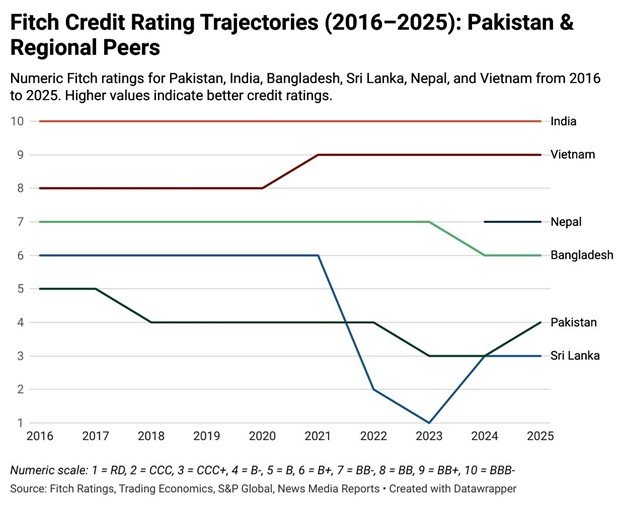

Pakistan vs Peers: Still Lagging Despite Progress

Despite the upgrade, Pakistan remains well below investment grade across all major rating agencies, with Moody’s and S&P yet to follow Fitch’s move.

The country faces substantial external debt repayments of $8 billion in FY25 and $9 billion in FY26, necessitating continued reliance on multilateral and bilateral financing sources.

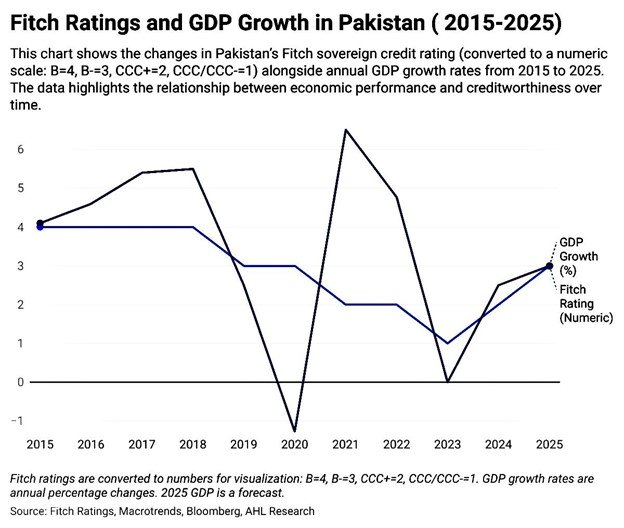

As shown in the chart below, Pakistan’s credit rating has fluctuated significantly over the past decade, with a notable downgrade to ‘CCC-’ in 2023 and now a recent upgrade, while most regional peers have maintained higher and more stable ratings.

Pakistan’s continued reliance on external financing highlights a key vulnerability, especially as financial reserves across South Asia remain limited after years of repeated shocks. While countries like Bangladesh and Vietnam have benefitted from stronger export performance and investment flows, Pakistan faces ongoing challenges in strengthening its fiscal position and mobilizing domestic revenues, according to the World Bank’s April 2025 South Asia Development Update.

Rating Agencies: Lagging Indicators or Valuable Signals?

Financial analysts often note that rating agencies tend to reflect past economic developments rather than predict future trends. Zafar Masud, former advisor to Pakistan’s Ministry of Finance, has argued in Dawn that the real challenge for Pakistan is to sustain fiscal discipline beyond short-term political cycles, a point that remains central as the country navigates recent upgrades and ongoing reforms.

Four Key Risks to Pakistan’s Economic Recovery

Despite recent progress, significant challenges threaten to derail Pakistan’s economic recovery:

1. Implementation Risks

Pakistan’s history with IMF programs shows reforms frequently stalling during political transitions. Fitch specifically notes in its April 15 press release that “ the current consensus on reforms could weaken as elections draw nearer and political volatility increases.”

2. External Financing Dependency

With limited capital market access. Pakistan remains heavily reliant on bilateral and multilateral financing to meet substantial debt obligations in FY 25-26.

3. Fiscal Fragility

The interest payment-to-revenue ratio is projected to reach 59% in FY25, severely limiting capacity for development expenditures or ability to absorb economic shocks. The latest IMF warns that without further reforms to broaden the tax base and reduce expenditure rigidities; fiscal sustainability remains at high risk despite current progress. The IMF acknowledges progress, including a 2.0% GDP primary surplus in H1 FY25 but emphasizes that sustained reforms are critical to address Pakistan’s narrow revenue base and high debt-servicing burden.

4. External Vulnerabilities

Ongoing global trade tensions and security concerns in regions bordering Afghanistan and in Balochistan continue to pose risks to export performance and investor confidence.

What’s Lies Ahead for Pakistan?

While Pakistan’s recent credit rating upgrade is a positive development,significant challenges remain before sustainable economic growth can be realized.Managing over $8 billion in external debt repayments due in FY 2025-26 will test the country’s fiscal resilience. Expanding the tax base and reducing dependence on external borrowing are essential steps to stabilize the economy and break the recurring cycle of financial instability.

Projected GDP growth of around 3% in 2025, according to the IMF,falls short of the 5-6% needed to meet the demands of Pakistan’s expanding labor force,as noted by the State Bank of Pakistan.

The upgrade should be viewed as a milestone rather than an endpoint. While the recent IMF review and credit rating upgrade represent important votes of confidence, they do not guarantee smooth sailing ahead. The IMF has specifically cautioned that Pakistan’s debt sustainability remains precarious, and further structural reforms are essential. Long-term progress hinges on consistent policy implementation, fiscal discipline and creating an investment friendly environment that can attract both domestic and foreign capital. Pakistan’s economic future depends not on temporary relief through external financing but on addressing fundamental structural weaknesses that have led to recurring cycles of crisis.

Sources

- Fitch Ratings, Pakistan Sovereign Credit Rating Upgrade Press Release, April 15, 2025

- Bloomberg, Pakistan Gains Credit Upgrade from Fitch, April 16, 2025

- Ministry of Finance, Pakistan Debt Sustainability Report FY2025-FY2027

- International Monetary Fund (IMF), World Economic Outlook, April 2025

- State Bank of Pakistan, Monetary Policy Statement, April 2025